COMPANY - REALTY INCOME CORP REIT

Ticker - O

What is it

Realty Income Corp owns roughly 13,400 properties, most of which are freestanding, single-tenant, triple-net-leased (A triple net lease is a lease agreement on a property where the tenant promises to pay all expenses, including real estate taxes, building insurance, and maintenance. These expenses are in addition to the cost of rent and utilities) retail properties. Its properties are located in 49 states and Puerto Rico and are leased to 250 tenants from 47 industries. Recent acquisitions have added industrial, gaming, office, manufacturing, and distribution properties, which make up roughly 17% of revenue.

How do they make money?

Over 80% of Realty Income's tenants are in the retail sector. However, most of these tenants operate in stable, defensive segments like service-oriented businesses that are not easily disrupted by online shopping or economic downturns. There leases are usually long-term, often lasting 15 years with extension options, ensuring a steady stream of rental income for the company. Tenants generally have high coverage ratios, indicating they are financially healthy and unlikely to ask for rent reductions even during economic slumps. This stability has helped Realty Income maintain a strong credit rating and remain part of the S&P High-Yield Dividend Aristocrats Index.

Despite diversifying its tenant base over time, approximately 40% of Realty Income's revenue still comes from its top 20 tenants. Any issues with these key tenants could negatively impact the company's revenue.

Opportunity

Realty Income recently completed a significant merger with Spirit Realty in January. Additionally, they acquired properties worth $598 million during the quarter. This included $16 million spent on five properties in the US with a 7.1% return rate, $302.6 million on eight properties in Europe with an 8.2% return rate, and $279.4 million on 142 developmental properties with an average return of 7.3% (Return rates are cap rates). While the higher returns in Europe are promising, these properties might carry more risk than those in the US, so Realty Income needs to be cautious about the number of European properties they acquire.

From 2018 to 2023, Realty Income sourced potential deals worth between $24 billion and $45 billion, mostly through existing relationships. They are highly selective, purchasing only about 5% of the deals they consider, demonstrating their focus on acquiring properties that add significant value. Due to a period of lower interest rates, they acquired over $23 billion in properties since 2021, showcasing their disciplined approach to growth.

Management

Realty Income’s management team is experienced and well-qualified. Sumit Roy has been the CEO since 2018, having joined the company in 2011 and previously serving as president, COO, and CIO. Christie Kelly became the CFO in January 2021, bringing prior CFO experience from Duke Realty. The senior management team and board members have experience in real estate and finance, ensuring effective management of the company.

Dividends

As you know probably the main reason people invest in REIT's is because of the dividend payouts. REITs, by law, have to pay out at least 90% of their annual taxable income as dividends.

The dividend started out at $2.40 in 2016 and has grown to $3.08 in 2024 with a 10-year average growth of +3.6%. That is average dividend growth and above the FEDs inflation target. And with their earnings being released for last quarter their coverage for those dividends is strong and a decrease is not likely. With a dividend coverage ratio at around .318 (Well below the 1-2 target) meaning this company does not have enough net income to cover all of their dividends paid to investors. However, this is not as big of a deal as it seems because they have Stable and growing cash flows over the past 10 years.

Performance

As you can see the company is down about 25% in the last 3 years and down about 26% in the last 5 years. The last few years have been very rough for REITs, so this can be a good sign that a good company is potentially underpriced.

Metrics

Metrics for REITs are all pretty much the same and the most important one is FFO or Funds from Operations. This analyzes the operating performance of REITs.

For the first quarter of 2024, Realty Income Corporation reported adjusted funds from operations (AFFO) of $1.03 per share. This figure met the consensus estimate and showed an increase from the $0.93 per share reported in the same quarter of the previous year. The company's total revenue for the quarter was $1.26 billion, which surpassed the estimated $1.19 billion, marking a 33.5% year-over-year increase

When looking at FFO you also need to look at Adjusted FFO payout ratio, which measures the FFO paid out as dividends. A rising ratio means dividends are growing faster than cash flow OR cash flow is declining. Below 90% is a good preference. ADC had an AFFO payout ratio of 88% in 2014 and projected 68.4% for this year meaning cash is growing faster than dividends. This shows that the company has improved its dividend sustainability over the last decade, providing a larger buffer to cover dividend payments and potentially allowing for future increases.

Other metrics to look at

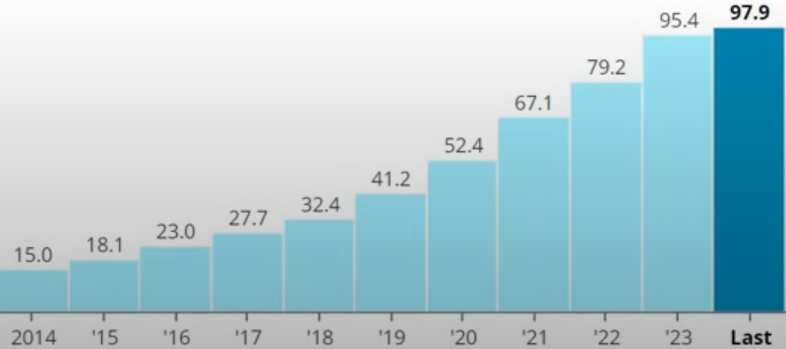

Revenue growth - Ave about 20% sales growth a year since 2019. 10% is a good benchmark.

Shares Outstanding (Millions) - 870.77M and the amount is increasing to help raise capital for expansion. Most REITs do this because they have to pay out so much of their income as dividends.

REITs normally have to issue shares and dilute your position to help fund growth because of the high-income payout.

Return on Invested Capital - Lowered from 4.47% to 2.67% from 2015 to 2024 and we want to see this number rising. ROIC is a gauge to watch how efficient management is at capital allocation so keep an eye on this.

Net Debt to EBITDA - (How many years of EBITDA a company would need to pay off all debt, net of cash on hand) For the first quarter of 2024, Realty Income Corporation's net debt to EBITDA ratio was approximately 5.3x and a target is below around 5.5 for REITs.

Wall Street Price Forecast

Current price 6/16/2024 - $53.30

Morningstar fair value - $76.00 (42.5% upside)

Refinitiv - $60.03 (12.6% upside)

Click the video ⬇️

Add comment

Comments